What is Electronic Money? Key Considerations

Electronic Money (e-Money) is the digital representation of a fiat currency stored electronically. It plays a key role in the modern financial system, especially for digital business models such as FinTech and e-Commerce.

Crucially, e-Money is neither a traditional bank deposit nor a cryptocurrency. Its unique characteristics and legal status create considerations for both corporate users and Electronic Money Institutions (EMI) providers.

Definition of Electronic Money

To be legally classified as e-Money, four characteristics must be fulfilled:

| Monetary Value | Holds a value equivalent to a fiat currency. |

| Stored Electronically | Is stored on electronic devices (prepaid cards or smartphone) or servers (digital wallet or online platform). |

| Accepted by Third Parties | Is accepted as a medium of exchange by entities other than the issuer. |

| Prepaid | e-Money is issued after receiving an equivalent amount of fiat currency in advance. |

Use cases of Electronic Money

Innovation is driving expanded use cases for e-Money:

| IBAN Issuance | Accounts with e-Money balances in a single or multiple currencies. |

| Neobanking | Bundled account, digital payment, FX, and card offerings. |

| Banking-as-a-Service | Offering account and payment services to 3rd parties in return for a revenue share. |

| Prepaid Cards | Cards loaded with a specific amount of e-Money and used for purchases later. |

| Digital Payment Platforms | Websites and apps for EMI to orchestrate online payments and hold balances. |

| Digital Wallets | Platforms like Revolut that store e-Money to facilitate online payments or money transfers. |

| Bank-Linked Digital Wallets | Wallets like Google and Apple Pay where e-Money is linked to bank accounts. |

| Mobile Money Services | Users store, send, and receive money using their mobile phones (M-Pesa). |

| Stored-Value Cards | Cards preloaded with e-Money and used for transportation or other services (Oyster). |

| Voucher Schemes | Users purchase vouchers online or at kiosks and redeem for online purchases (PaySafeCard). |

Why does Electronic Money matter

Since 2000, e-Money has developed to play a key role in the modern financial system:

| eCommerce | e-Money acts as an efficient alternative to traditional banks and payment rails. Being natively digital, it seamlessly integrates into other systems, creates rich data, and supports real-time value transfer. |

| EMI | Low regulatory barriers (relative to banking) enable agile FinTechs to disrupt financial services. Whilst EMI market share remains modest, growth prospects are strong as the industry matures. |

| Regulators | e-Money has created choice for consumers, reduced dependency on the banks, and provided learnings for crypto, stablecoin, and central bank digital currency (CBDC) innovation. On the downside, e-Money is subject to financial crime and rated high risk in national risk assessments. |

How Electronic Money compares to Bank Deposits and Crypto

It is essential to understand the nuances and legal ramifications of different types of money:

| Feature | Electronic Money | Bank Deposit | Crypto |

| Backed by Fiat | Yes | Yes | No |

| Interest Bearing | No | Yes | No |

| Protection | Safeguarded | Guaranteed to a limit | None unless collateralised |

| Regulation | Electronic Money Directive (EMD) | Banking Acts | Markets in Crypto Assets (MICA) |

NB. Europe as as Q3 2025, market subject to change.

How large is Electronic Money in Europe

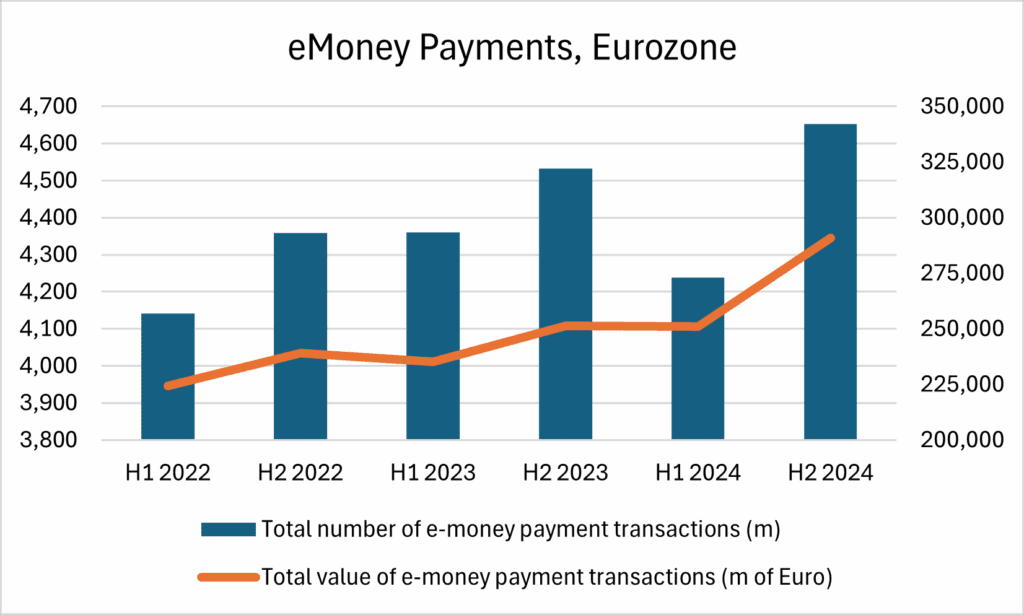

Data from the European Central Bank (ECB) demonstrates the rapid scaling of e-Money in the Eurozone:

Transaction Volume: 4.6bn in H2 2024, up 2.6% on prior year.

Total Value: EUR 0.3 tn, up 15.8% on prior year.

Market Share: e-Money payments account for 5.97% of total payments in the Eurozone.

Active Players: At the time of writing, there are 325 authorised EMI in the EU.

How is Electronic Money Regulated in Europe?

Regulation of e-Money in the EU is primarily governed by the Electronic Money Directive 2 (EMD2).

Authorisation is required by the competent authority of the Member State where the applicant is established, after which “Passporting” to all EU countries is possible on approval.

Obtaining an EMI license is an extensive 9-18mths process. Applicants must possess a sustainable business plan, robust operating plans, technology infrastructure, experienced team, initial capital of €350000, local substance, customer conduct policies, governance structures, AML/KYC monitoring, client funds safeguarding, and an ongoing compliance program.

What is Electronic Money Safeguarding?

An EMI must separate client funds from their own funds. The requires the EMI to place client funds into a special segregated account with a highly rated bank, or hold alternative insurance or guarantees.

If the EMI fails, safeguarded funds are not part of the EMI assets and returned to clients in the insolvency procedure.

If the safeguarding bank fails, funds are protected by the statutory deposit guarantee scheme and returned to clients in the insolvency procedure.

Strategic considerations for Electronic Money

Corporate

| Pros | e-Money is convenient, especially for digital business models, and often enables quicker and cheaper payments. |

| Cons | e-Money balances are not interest-bearing and not covered by deposit guarantee schemes. |

| Risks | EMI may be thinly capitalized and unrated, making counterparty risks assessment vital. |

EMI

| Scale | Set-up costs are significant and competition high, volumes are required to break even. |

| Infrastructure | Good client engagement, regtech, and core banking technology are required to process efficiently at scale. |

| Regulation | Regulatory requirements for EMI are increasing, as are enforcements for non-compliance. |

| Partnering | Securing partners for safeguarding is lengthy due to AML/CTF risk. The flow and accounting of transactions must be precise. |

| Risk Management | Treasury skills are crucial to manage liquidity, counterparty credit, market and legal risks. |

Electronic Money Summary

e-Money has secured its place in modern financial infrastructure due to its flexibility, convenience, and efficiency. Innovation, real-time payment demands, and the growth of eCommerce will drive further adoption. Challenges exist, including the fight against financial crime and new regulatory requirements such as AML, DORA and, soon, PSD3. Early-stage consolidation is occuring and only the most efficient and compliant EMI will thrive.

How Sure FinTech Helps

Sure FinTech provides a range of services to help clients navigate the ekectronic money landscape:

| Corporates | FinTechs |

| Understand the e-Money opportunity and connecT with EMI providers. | Develop strategy, secure EMI authorisation, and procure enabling financial technology. |

Contact Us today for a free consultation.