What is Electronic Money? Considerations for Corporates and EMIs

- Electronic Money is the digital representation of a fiat currency that is stored electronically.

- Electronic Money is prepaid and can be redeemed for cash or other payment transactions.

- Electronic Money has emerged to play a crucial role in the financial system and ecommerce.

- Electronic Money is neither a deposit nor a cryptocurrency.

- The unique legal and regulatory status of e-Money creates considerations for users.

Definition of Electronic Money?

To be classified as e-Money, certain characteristics must be fulfilled:

- Monetary Value: it holds a value equivalent to a fiat currency.

- Stored Electronically: it is stored on electronic devices (prepaid card or smartphone) or servers (digital wallet or online platform).

- Accepted by Third Parties: it is accepted as a medium of exchange by entities other than the issuer.

- Prepaid Nature: e-Money is issued only after receiving an equivalent amount of fiat currency in advance.

What are examples of Electronic Money?

- IBAN Issuance: accounts with e-Money balances in a single or multiple currencies.

- Neobanking: bundled offer of accounts, digital payments, FX, cards, etc, often augmented with software for easy management.

- Banking-as-a-Service: offering account and payment services to 3rd parties on your infrastructure in return for a revenue share.

- Prepaid Debit Cards: cards that are loaded with a specific amount of money and can be used for purchases later.

- Digital Payment Platforms: websites and apps that orchestrate online transactions and may hold a balance for users.

- Digital Wallets: platforms like PayPal and Revolut that store e-Money to facilitate online payments or money transfers.

- Bank-Linked Digital Wallets: wallets like Google Pay and Apple Pay, where e-Money is linked to bank accounts.

- Mobile Money Services: allows users to store, send, and receive money using their mobile phones, like M-Pesa.

- Stored-Value Cards: cards like Oyster, which are preloaded with money and used for transportation or other services.

- Voucher Schemes: uers purchase vouchers online or at kiosks then user them to redeem for online purchases, like PaySafeCard.

Why does Electronic Money Matter?

For corporates, e-Money is an alternative to traditional bank accounts and payment rails. e-Money is flexible and able to cover numerous use cases, currencies, and enable real-time transactions. Often cheaper than traditional banking services, e-Money does not qualify for deposit guarantee schemes.

For FinTechs, low regulatory barriers to entry have made it possible to disrupt the financial services industry. Although the market share remains modest, growth forecasts are strong, and valuable unicorns such as Revolut have been formed, while others, such as Wise have floated.

For Regulators, e-Money has created choice for consumers, reduced dependency on the banks, and provided learnings for cryptocurrency, stablecoins, and central bank digital currency (CBDC) innovation. However, e-Money is subject to high levels of money laundering and digital payment fraud, and EMIs are typically rated as high risk in national risk assessments.

Is Crypto the same as e-Money?

No. Cryptocurrency and stablecoins are digital money however they are not tied to fiat currencies nor backed by any central authority. Crypto assets are subject to separate legal status and regulation.

Is a Bank Deposit e-Money?

No. Bank accounts do hold fiat currency electronically, but are subject to separate legal status and regulation. Bank deposits qualify for state deposit guarantee schemes, e-Money does not, but is safeguarded.

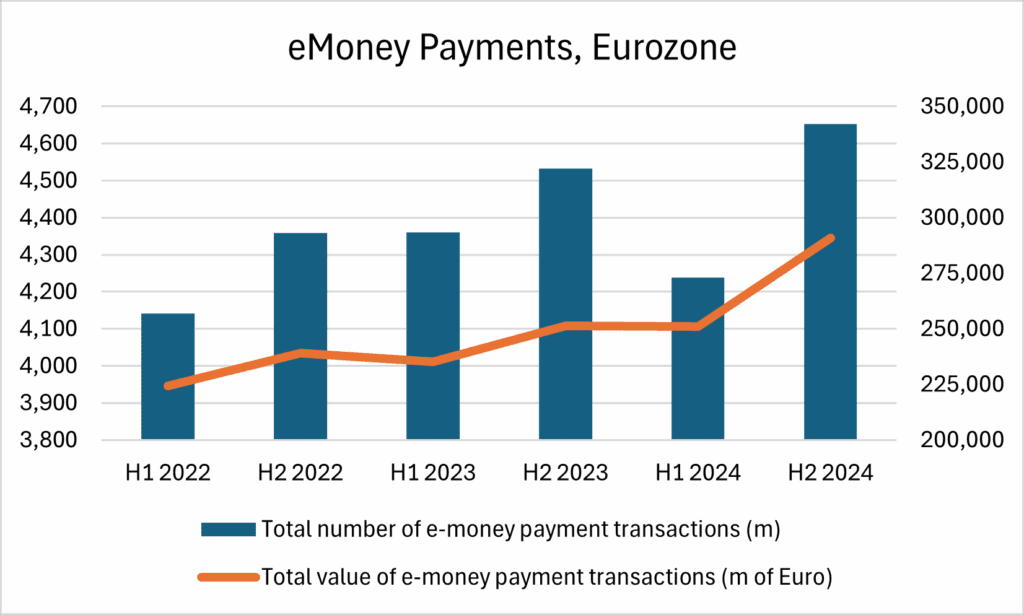

How large is Electronic Money in Europe?

According to the European Central Bank, the number of e-Money transactions in the Euro area in H2 2024 was 4.6bn, up 2.6% on the prior year. Total value was €0.3 tn, up 15.8% on the prior year. e-Money accounts accounted for 95% of volume and 93% of value, while cards accounted for 5% and 7% respectively.

e-Money payments account for 5.97% of total payments in the Eurozone.

At the time of writing, there were 325 authorised and active EMIs in the EU.

How is Electronic Money Regulated in Europe?

The regulation of e-Money in the EU is primarily governed by the Electronic Money Directive 2 (EMD2).

Authorisation for e-Money services is provided by the competent authority in the Member State where the applicant is established. Passporting to additional EU countries is possible on approval.

Applicants must meet robust requirements including a sustainable business plan, robust operating plans, technology infrastructure, experienced team, initial capital of €350k, local substance, customer conduct policies, good governance structures, AML/KYC monitoring, client funds safeguarding, compliance program.

The process is extensive, 9-18mths depending on the services and jurisdiction. Applicants are expected to have capabilities in place if not operational at time of application.

What is Electronic Money Safeguarding?

EMIs are required to safeguard client funds by keeping them separate from their own operational funds. The requires the EMI to place client funds into a special segregated account with a highly rated bank or have alternative insurance or guarantees.

If the EMI fails, safeguarded funds are not part of the EMIs assets and are returned to customers via the insolvency procedure.

If the safeguarding bank fails, the funds are protected by the statutory deposit guarantee scheme up to €100k, provided the bank is covered by the scheme. Return of the funds is subject to insolvency procedure.

e-Money Considerations for Corporates

- e-Money is convenient, allowing for quicker and cheaper transactions, especially in ecommerce and international use.

- e-Money balances are not interest-bearing.

- e-Money is not covered by state deposit guarantee schemes in the way that bank deposits are.

- EMIs are usually thinly capped and unrated, meaning they do not meet treasury policies

e-Money Considerations for EMIs

- Good client engagement, regtech, and core banking technology are required to process efficiently at scale.

- Regulatory requirements for EMIs are increasing, as are enforcements for non-compliance.

- EMIs must understand ideal client profiles and lifetime economics.

- Securing partners for client funds safeguarding is lengthy and difficult due to AML/CFT risk.

- Treasury management skills are required to manage liquidity and counterparty credit risk.

- Are safeguarding or banking-as-a-serve partners disclosed?

- Are safeguarding or banking-as-a-serve able to account for revenue share?

- Is the flow of client funds between EMI and safeguarding partner smooth?

Electronic Money Summary

e-Money has established itself as a key component of the financial system due to its flexibility, convenience, and efficiency. Innovation, real-time payment infrastructure, and growth in the global digital economy will drive further adoption. Challenges exist, including the fight against money laundering and digital payment fraud, thus it is reasonable to assume EMIs will face increased technological and regulatory requirements in the coming years, ultimately leading to consolidation of the sector.