The credit card payment journey: Key players and risks

- Credit cards are favoured by buyers due to their convenience for payments and unsecured credit.

- Credit cards are a significant and growing market globally.

- Multiple stakeholders and risks are involved in the credit card payment journey.

- Merchants are often settled weeks after the transaction.

- Global credit card payments and are huge and growing.

Why do credit cards matter?

Credit cards are a huge market. In the US, they are the dominant payments method, accounting for 31-40% of total with an annual value of USD 5tn. 800m credit cards are in circulation with total debt exceeding USD 1.2 tn, the average cardholder has 3.9 credit cards and USD 6.7k debt.

In the UK, 56% of adults own a credit card and make 5bn payments annually.

Given the interest rates and interchange fees charged, credit cards provide high profitability and support a large industry of financial services and technology providers.

What is the credit card payment journey?

The credit card payment journey, from purchase to merchant being settled, involves multiple steps and stakeholders.

Costs to cardholders include the monthly card fee and interest on borrowed amounts, while merchants pay service fees including interchange.

Although payments occur in real-time, final settlement of cashflows is significantly later.

Risks, including payments fraud, chargebacks, IT failure, and credit exist.

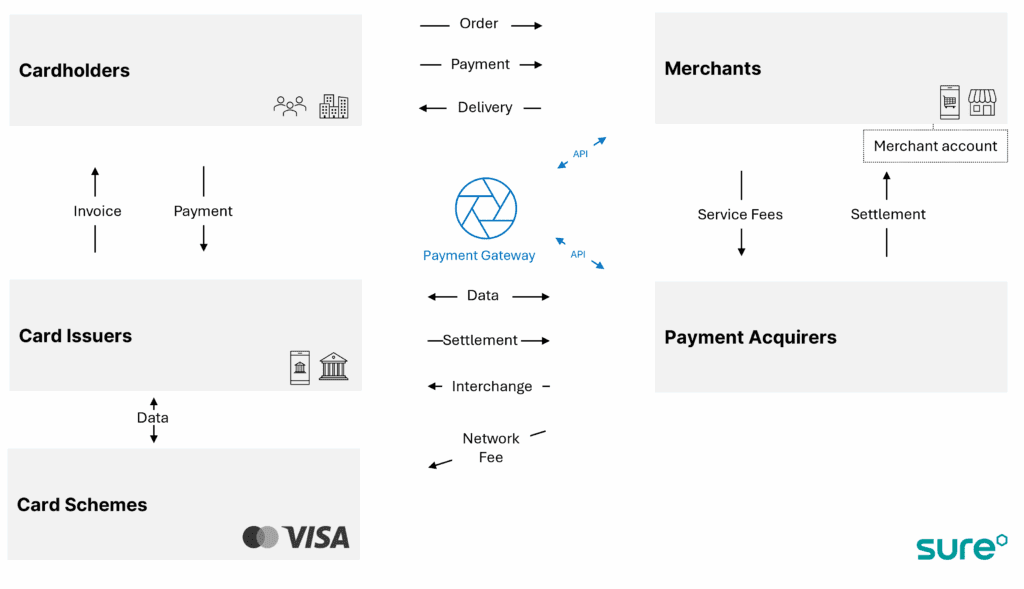

Who are the parties in a credit card payment?

Cardholders are consumers and corporates (corporates pay more for credit cards).

Merchants and marketplaces are sellers of goods and services, through e-Commerce or POS.

Payment Acquirers are regulated payment service providers who act as agents of the card issuer and schemes.

Card Issuers are banks and fintechs that market cards.

Card Schemes sponsor the card network, set rules, and interchange fees.

Technology providers like payment gateways connecting the ecosystem with real-time integrations to merchants and acquirers.

New models like payment orchestration emerge, where one player plays multiple roles to capture greater share.

What is the process of credit card payments?

- Cardholder presses pay on Merchant website.

- Data is transferred to Gateway where is it tokenised.

- Transaction is routed by Gateway to Acquirer in encrypted form.

- Acquirer sends message to the Issuer to verify.

- Issuer confirms with Card Scheme that Cardholder is legitimate (authentication) and funds are available (authorisation).

- Card Scheme passes response to Issuer and Acquirer.

- Acquirer sends success/fail message to Gateway.

- Gateway sends success/fail message to Merchant.

- Merchant website sends success/fail message to Cardholder.

- Merchant is paid in arrears by Acquirer, net of chargebacks, fees, reserve adjustments.

- Gateway charges Merchant separate fee.

Common problems in the credit card payment journey

Errors are possible, although in practice, businesses monitor performance using metrics such as conversion ratio, acceptance rate, disputes, chargebacks, losses to fraud, and technology error codes.

Cardholders

Card detail error or expiry.

Fails two-factor authentication.

Insufficient limit.

Merchants

Fails PCI-DSS requirement.

Unreliable technology.

Payment Acquirer

Transaction declined as suspect (amount, location, currency, pattern, etc).

Transaction fails velocity check.

Risks in the credit card payment journey

Payment Fraud

Financial crime affects cardholders, PSPs, and issuers. Mastercard estimates global eCommerce losses to fraud total USD 50bn annually and expects this to rise as criminals embrace technology to stage elaborate phishing, identity theft, and account takeovers.

Chargebacks

Customers often dispute payments. Most are settled amicably, but instances of chargeback fraud occur when the cardholder cancels the payment with the card issuer, leaving the merchant with a loss. If a merchant has a history of chargebacks, the issuer will retain a rolling reserve to cover such eventualities.

Credit Risk

Credit risk occurs when a counterparty does not settle their obligation, in full, when due. As settlement occurs in arrears, there is risk in the credit card payment journey, notably between Issuer-Cardholder and Merchant-Acquirer (albeit they are usually large and regulated).

Technological Failure

Processing credit card payments requires integration of web and mobile apps, payment gateways, tokenisation, and payment acquirers. Failure of an element will result in cart abandonment or failed payments. Each element, and the data therein, must be secured in accordance with Payment Card Industry Data Security Standard (PCI-DSS) requirements.

Summary of the credit card payment journey

Credit cards provide access to unsecured debt and are convenient for payments. Volumes are expected to grow in all major markets, making them a vital element in any payments mix.

As the credit card payment journey illustrates, the industry is complex, raising concerns about opacity, cost and settlement speed.

Innovation is creating competition and alternative payment methods, thus merchants and PSPs must retain focus while taking opportunities to optimise their partners, processes, and technologies.