How to choose a Banking-as-a-Service provider

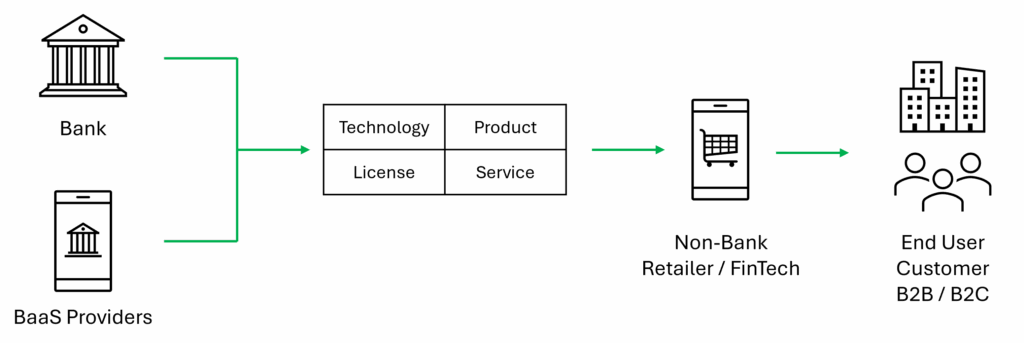

Banking-as-a-Service (BaaS) is when an authorised financial institution allows a non-bank to offer financial services on its infrastructure.

BaaS lowers barriers to entry in financial services but creates investment and compliance obligations.

The models available, their financial and practical implications are often misunderstood.

Clarifying key elements at the outset leads to better business fit, economics and creates an enduring partnership.

Here are 6 ways to assess a Banking as a Service provider:

Banking-as-a-Service Product Fit

Financial services are competitive, and end-user clients rarely switch quickly, so having a compelling offer is essential.

Non-banks should assess product availability by market, including what currencies and payment rails are supported.

Banking-as-a-Service Risk Appetite

BaaS providers create risk ratings based on criteria including country, industry, transaction profiles, end-user clients and UBO.

High-risk business may be excluded, subject to additional checks, or priced higher.

It is also important to understand how often risk policies are reviewed, what is accepted today may not be in 6mths.

Banking-as-a-Service Licensing

BaaS providers are licensed to ensure consumer protection, market stability, and operational resilience.

Historically, non-banks could act as agents or resellers however, the trend in Europe is that all parties must be licensed, which involves extra time and requirements.

Card products have additional considerations about BIN sponsorship and PCI-DSS.

Banking-as-a-Service Technology

Fintech directly influences client experience, operating efficiency, compliance and adaptability.

BaaS providers will have a specific configuration for client engagement by web/mobile, regulatory technology for KYC/KYT, and core banking for transaction and back-office processing.

Non-banks may bring their own technology and connect via API, providing more control over features, roadmaps, and development priorities.

Banking-as-a-Service Revenue Model

Each BaaS provider will have a specific model based on implementation cost, monthly minimum fees, and transaction revenue sharing.

Financial services are profitable at scale, but non-banks must ensure their assumptions about growth and expenses are modelled correctly.

Banking-as-a-Service Processes

BaaS requires mutual effort to onboard business, deliver profitability, and meet compliance obligations.

Responsibilities and service levels should be clearly defined in advance, with thought given to end-users.

Processes around KYC, accounting, and funds safeguarding merit additional focus due to their significant impact.

BaaS Summary

BaaS is growing in Europe, especially for digital business models such as eCommerce and FinTech, which can unlock scalable growth on cost-effective infrastructure.

Nonetheless, non-banks often misunderstand key aspects of BaaS, which are also subject to rapid change.

Taking advice early and working with a framework will lead to better decisions, easier go-to-market, and sustainable profitability.