Open Banking in Europe

Open Banking emerged as a concept in 2010s, as regulators sought to stimulate competition and innovation in financial services.

On launch in 2018, adoption was slow as fragmented technology, concerns about data sharing, and limited use cases created headwinds.

Over time, the popularity of digital business models such as fintech and ecommerce grew among consumers and businesses.

Third-party providers (TPPs) emerged to innovate new services, improve processes, and enable decisions that were previously excluded.

Trust in the Open Banking ecosystem has grown as customer protection, regulation and financial technology have matured.

How large is Open Banking Europe?

According to Konsentus, there were 554 authorised TPPs in Europe in Q4 2025. The UK is the single largest market with 193, followed by Germany 32, France 31, and Sweden 28.

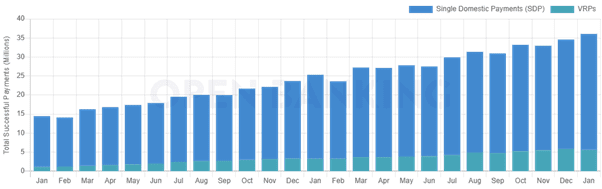

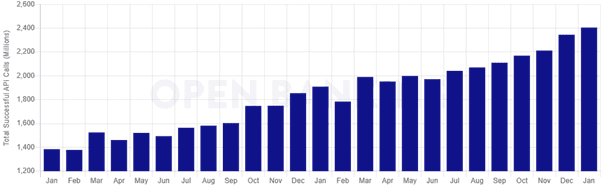

Regulators estimate the UK has 16m Open Banking users, and 2025 saw a “significant shift in how consumers and businesses manage their finances” as payments rose 53% year on year. This is borne out by industry data for 2025:

EU data is lacking. Whilst PSD2 sets a standard, each jurisdiction implements slightly differently, creating fragmentation and lack of uniform reporting.

How is Open Banking regulated in the EU?

Payment Services Directive 2 (PSD2) is the primary legislation.

TPPs must be authorised for Payment Initiation or Account Aggregation. This ensures standards, that data is secured by technological and operational means, and consumers are protected.

Payment Initiation Service Providers (PISPs) are permitted to initiate payments directly from a customer’s account.

Account Initiation Service Providers (AISPs) are permitted to aggregate information from multiple accounts to gain a comprehensive view.

Other regulations considered include the General Data Protection Regulation (GDPR), Regulatory Technical Standards (RTS), and Digital Operational Resilience Act (DORA).

Market participants are preparing for PSD3, Payment Services Regulation (PSR), and Financial Data Access (FIDA) Regulation. This should encourage further innovation and harmonise the market.

How is Open Banking regulated in the UK?

Open Banking in the UK is regulated by the Financial Conduct Authority (FCA) and the Payment Systems Regulator (PSR).

Payment Services Regulations 2017 is the primary legislation.

Despite Brexit, the principles remain close to the EU.

The UK seeks growth in Open Banking by innovating new services such as open banking payments for e-commerce and variable recurring payments. Independent industry body Open Banking Limited acts as a catalyst.

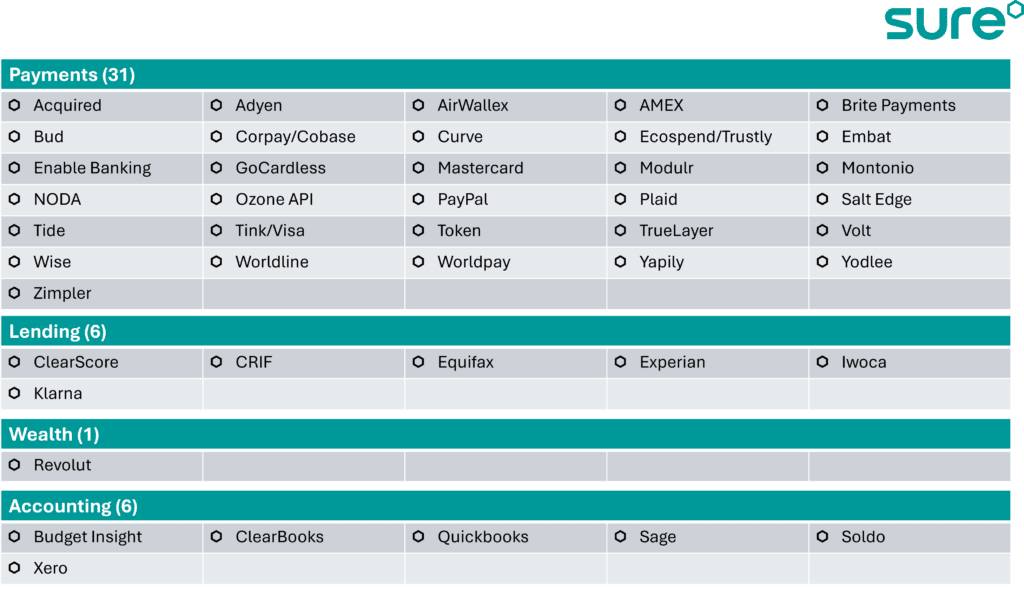

Open Banking providers in Europe: Payments lead

Sure tracks 44 significant open banking providers in Europe, with up to a further 150 active:

Payments remains the largest segment, with lending, accounting, wealth, insurance and fraud all expected to grow.