What are Interchange Fees and why do they Matter?

Interchange fees are the transaction costs applied to a merchant when a customer makes a card payment. The sums are significant, several % per transactions, and in 2023 US merchants paid USD 135bn in interchange fees. Whilst this funds investment in the card scheme, it attracts criticism from regulators and competition from FinTechs targeting profits with alternative payment methods.

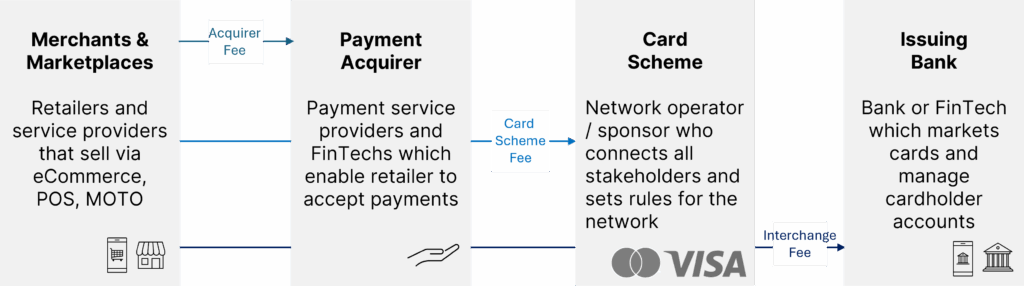

Parties in a card payment

It is important to understand the card payment process, as interchange fees are collected by the payment acquirer and apportioned between the card issuer, card scheme and payment acquirer:

How is a card payment charged?

Contrary to popular belief, the proceeds are not retained by a single party but split across the payment ecosystem. Here is how an EUR 100 card payment may be apportioned:

Why the Payments Industry is obsessed with Interchange

The value of interchange is massive and growing, even as alternative payment methods emerge:

| Credit Cards | Global market was estimated at USD 558bn in 2023, and may grow to USD 1.15tn by 2033. |

| Debit Cards | Global market was valued at USD 95bn in 2023 and is projected to reach $151bn by 2032. |

| Interchange Fees | The Banker estimates that US merchants paid USD 135bn in interchange fees in 2023. |

How is interchange calculated?

Interchange fees are set by the card scheme, like Visa and Mastercard. The interchange fee charged comprises many elements:

| Card Scheme | Each card scheme has a slightly different rate. |

| Card Type | Credit card payments have higher interchange fees than debit or prepaid because delayed settlement involves credit risk. |

| Payment Channel | Payments vary across channels such as eCommerce, POS and MOTO. |

| Industry | High-risk Merchant Category Code industries like travel, gambling, and charity pay more. |

| Customer Segment | Corporate cards are exempt from price caps and face higher interchange fees than consumer. |

| Location | Cross-border and/or currency fees apply if the card payment is made in a country different to where it was issued. |

Why is interchange controversial?

Interchange is criticised as it is opaque, non-negotiable and in some cases significant:

| Merchants | Merchants see the cost of interchange but may not understand how it is calculated. Small merchants pay more than large as they lack economies of scale. |

| Cardholders | Buyers may not know the interchange fee or when it has been passed on to them by the merchant. |

| Regulators | Regulators are unhappy about the lack of transparency. Some cards offer rewards for higher spending, which entices cardholders to take on high-cost credit, with the reward being financed by interchange e.g. the consumer pays twice. Regulators cite card schemes and issuing banks for abuse of power as they hold large market shares. |

Regulation of interchange fees

The card payment market is regulated for data security and pricing:

| EU | Interchange fees are capped at 0.2% for consumer debit/prepaid cards, and 0.3% for consumer credit cards by PSD2. |

| US | Interchange fees of 2% are typical. The Credit Card Competition Act (2022) to break the Visa-Mastercard card scheme duopoly and save merchants-consumers money is subject to intense lobbying. |

How does FinTech affect the Cards industry?

FinTech is driving rapid change across the global payments industry:

Account-to-Account Payments

A2A payments involve the direct transfer of funds from one bank account to another, bypassing a card scheme entirely.

Open Banking

Open Banking provides APIs that allow merchants to connect to multple payment rails and enable 3rd party payment initiation.

PayFac Model

Companies like Adyen play multiple roles. PayFacs utilise technology to improve engagement, embed payments and credit into eCommerce, and offer APIs that enable automation.

Banking-as-a-Service

BaaS allows non-banks to offer financial services. In recent years this has seen the emergence of payment service providers specialising in niches such as card payment.

Alternative Payment Methods

APMs like digital wallets (Google/Apple), PayPal, “buy now, pay later” (BNPL), and crypto payments become accessible to merchants.

Interchange Summary

The payment landscape has altered significantly in the past decade as regulation, technology and customer demands impact the payment mix. Nonetheless card payment remains favoured for convenience and is forecast to grow. Alternative providers emerge but card scheme power remains strong, indeed they increasingly acquire to consolidate the payments industry. Interchange fees will therefore remain significant for decades.

How Sure FinTech Helps?

Sure FinTech provides a range of services to help merchants and PSPs:

| Merchants | PSPs |

| Secure processing and analyse your history to understand if rates are appropriate. | Connect with merchants, secure regulatory licenses and source new technologies. |

Contact Us today for a free consultation.