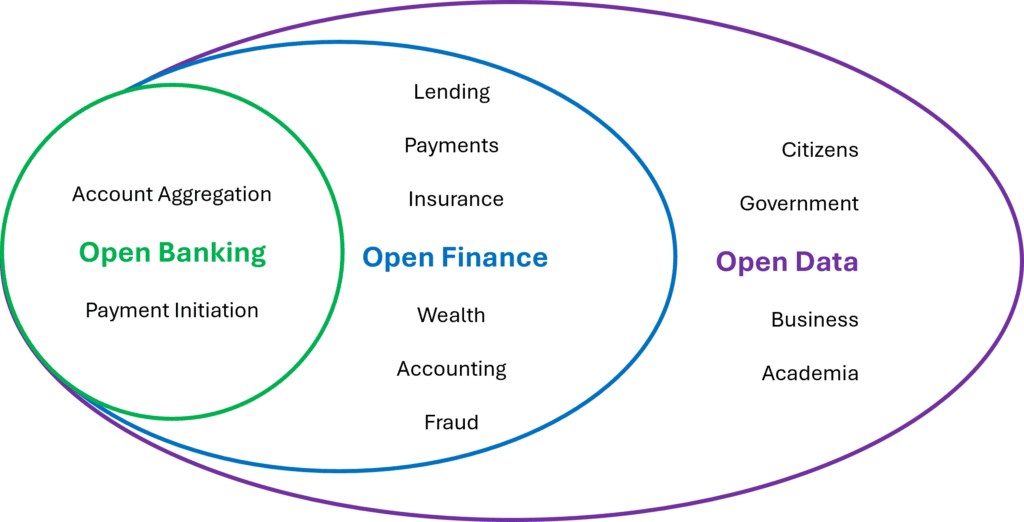

What is Open Banking? Beyond Payments

Open Banking allows third-party providers (TPPs) to source account data and initiate payments from a customer’s account at another financial institution.

Open Banking is used by financial and non-financial businesses to innovate new services, automate processes, and make decisions that were previously excluded, giving customers better choices and experiences.

Consumers and businesses must consent to their data being shared with the TPP, who in turn must be regulated.

Types of Open Banking

Payment Initiation

Payment Initiation Service Providers (PISPs) are permitted to initiate payments directly from a customer’s account.

Account Aggregation

Account Initiation Service Providers (AISPs) are permitted to aggregate information from multiple accounts to gain a comprehensive view in one place.

Open Banking Use Cases

Payments

Whether paying a bill or buying online, payments are embedded in the commercial process, making reducing friction for consumers and helping businesses increase conversions.

Lending

Lenders can verify income and expenses in 3rd party accounts. This allows them to make credit assessments in real-time to support online lending, embedded credit such as buy now, pay later (BNPL) and complex loans.

Insurance

Insurance companies can enrich their dataset and identify patterns, making it easier to assess coverage, provide customised offers, and price risk.

Wealth

Open Banking provides insights for budgeting and enables sweeping of excess balances to savings and investment products, either as a single or recurring payment.

Accounting

Finance platforms utilise Open Banking to match invoices issued/paid to bank account movements, improving AR/AP processes and working capital.

Fraud

The ability to analyse data and request authentication allows businesses to identify fraud faster and reduce the risk of loss.

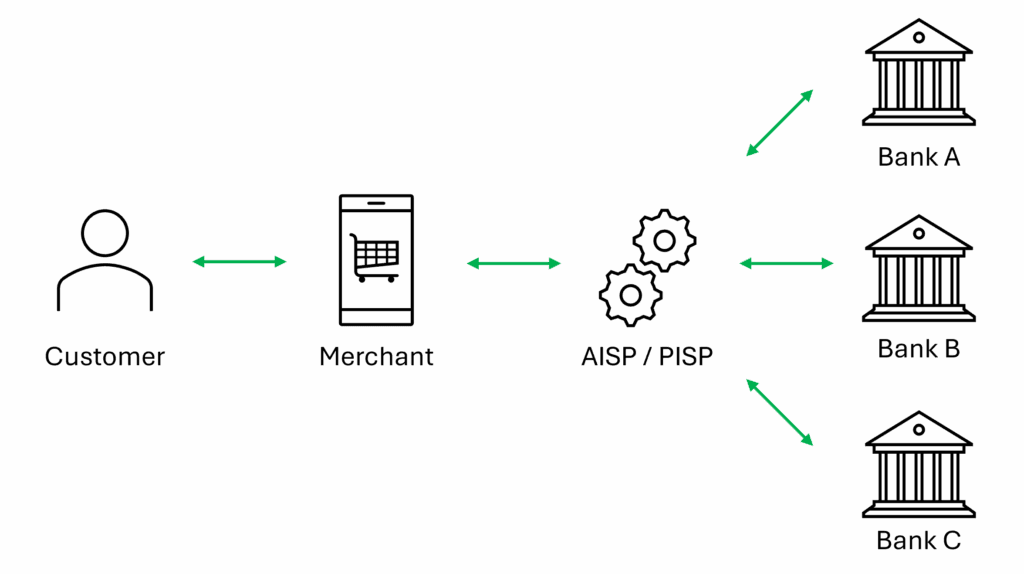

How does Open Banking work?

Open Banking relies on Application Programming Interfaces (APIs) to pass standardised data between the AISP/PISP and financial institution(s) in a secure manner.

APIs enable technologies to integrate, in real-time with business rules and protocols applied, to make the transaction is seamless.

Open Banking requires a customer’s consent, which must be verified by entering their bank login credentials when prompted.

Once the bank verifies the user, it generates an encrypted token that identifies the customer but does not expose their credentials.

To enable the transaction, the customer must authenticate the transaction, with a second token issued to complete the transaction.

Use of strong customer authentication (SCA) and tokenisation protects against financial crime.

Benefits of Open Banking

Open Banking fosters competition in financial services by allowing TPPs to access data and initiate payments.

Digital business models, like ecommerce and fintechs, use this to build enhanced capabilities, including decisioning, processes to products. Revenues are increased and risks reduced.

Open Banking users generate deep insights on their finances and receive personalised offers with seamless user experiences. Open Banking can deliver lower payments costs, yield maximisation, access to credit, and time savings.

Problems with Open Banking

Not all Banks support Open Banking, typically due to concerns about data privacy and granting third-party access.

Not all customers are happy about data sharing. Although consent must be given and authenticated, concerns about inappropriate usage exist.

Participants require good technology, including a good core banking or payments system which can operate securely in real-time, and CRM capability to manage consents

Open Banking Summary

After slow adoption, Open Banking in Europe is growing as measured by active users, payments volumes and API calls.

Further growth is expected due to positive regulatory factors, IT interoperability, and additional usage in digital business models.

Fragmented technology and financial systems can limit application, but customers expect personalised offers with seamless experiences, creating a business case on which to build.