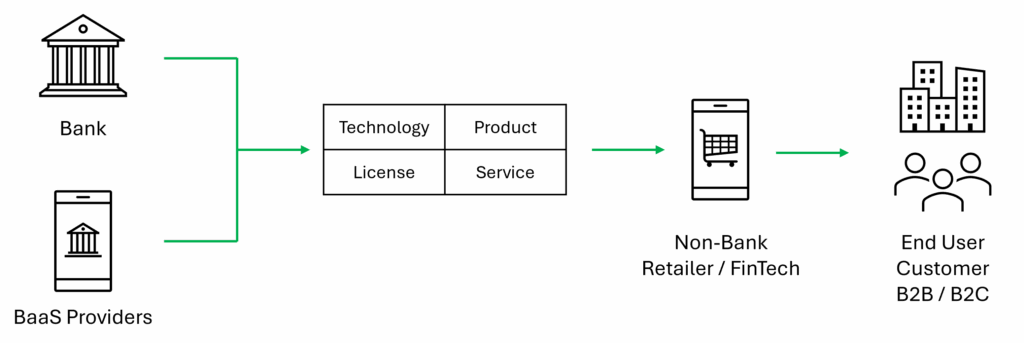

What is Banking as a Service?

Banking as a Service (BaaS) occurs when an authorised financial institution allows a non-bank business to offer financial services on a white-label basis.

This allows the non-bank to creatie new revenue streams, better customer experiences and deeper relationships.

BaaS lowers the barrier to entry to financial services and is profitable at scale. However, it remains a strategic consideration, given the upfront resources and compliance required.

Types of Banking as a Service

Product Specific

The BaaS provider offers a specific product like accounts, payments, FX, lending, or investments.

Neobanking

Products are bundled to create a neobank, which serves customers through the digital channel.

Full Stack BaaS

The BaaS provider extends its infrastructure – technology, regulatory license, compliance, client service and other capabilities – to provide a bank-in-a-box.

IT Infrastructure

The middleware model involves the BaaS provider extending its superior technology to a non-bank or financial institution. Examples include client engagement, KYC, trading, and core banking.

Aggregator

Connects non-bank to multiple financial institutions using a single API integration. This allows the non-bank to access rich data and embedded services in a standardised manner, reducing IT and compliance complexity.

Banking as a Service use cases

Embedded Credit

Offering loans and consumer credit like Buy Now, Pay Later (BNPL), often utilised by retailers to increase average sales size.

Embedded Insurance

Popular in POS and eCommerce, embedded insurance allows a retailer to cross-sell cover for high value purchases.

Payment Processing

Offering payments and foreign exchange, often utilised in eCommerce to offer a buyer more payment options and ensure increase conversions.

Accounts

Providing IBANS and digital wallets, allowing businesses to hold funds in eMoney form, offer loyalty rewards, and integrate payments.

Investments

Providing deposit, trading and investment products, including budgeting apps to identify excess balances and auto-sweeping for yield maximisation.

Card Issuing

Providing white-labelled debit, credit and prepaid cards for travel, expenses, procurement, rewards, etc.

Embedded Banking

Products are bundled to create a neobank, which serves customers through the digital channel only.

Benefits of BaaS for Businesses

Customer Experience

BaaS allows financial services to be embedded in a digital platform or process. Customers receive an offer when they need it, streamlining the process and increasing conversions.

Revenue Generation

Businesses add new revenue streams to core products, increasing and diversifying profitability. Done correctly and at scale, financial services offer high profitability.

Customer Loyalty

The ability to give personalised offers and good user experiences drives retention and higher lifetime value, rewards are often shared with clients to create a virtuous circle.

Go to Market

Leveraging the expertise and infrastructure of an authorised BaaS provider makes it easier, faster and cheaper to offer financial services than doing so alone.

How does Banking as a Service technology work?

BaaS is a financial technology business model which relies on Application Programming Interfaces (APIs) to securely integrate technologies.

Standardised data passes between the BaaS provider, business, and end user in real-time.

Strong customer authentication (SCA) verifies users and authenticates transactions, with data passed in tokenised form to protect against financial crime.

Business rules are applied to ensure that transactions meet regulatory and internal requirements for AML/CTF.

The exact technology stack will vary however there are 3 key components in the technology stack:

| Client Engagement | RegTech | Core Banking |

| Clients initiate service and communicate through a mobile application and/or internet bank. | Mandatory AML/CTF and business rules are applied at onboarding, funds in/out, review, etc. | Manage client records, communication, product configuration, transaction processing, workflow management, general ledger accounting and reporting. |

How is BaaS regulated in the EU?

BaaS providers must be authorised, typically as a Bank or eMoney Institution.

Non-bank businesses are typically licensed as a Payment Institution or eMoney Institution. Variations exist, including Payment Agent and eMoney Distributor, as do junior licenses.

Both parties have ongoing compliance obligations including AML/CTF, reporting on client funds and financial performance, digital operational resilience, and client conduct.

It is essential to understand legal and regulatory requirements in advance.

Problems with Banking as a Service

Regulatory scrutiny is increasing on payments and collections on behalf of third parties (POBO/COBO) as they can be misused for financial crime.

Regulatory scrutiny is increasing on the financial strength of BaaS participants. Failures and inaccurate accounting of client funds have occurred, resulting in enforcements and losses.

Whilst BaaS streamlines access to financial services, it still requires businesses to have some capability in technology, compliance, and service. Revenues are shared, and volume is required to be profitable.

The non-bank business is dependent on the risk appetite of the BaaS provider, which changes, it is essential to meet the risk and reporting requirements to secure reliable service and pricing.

Banking as a Service Summary

After rapid early adoption, Banking as a Service in Europe has matured as businesses, providers, technology and regulation have evolved.

Further growth is expected, especially for digital business models such as eCommerce and FinTech where BaaS creates high value.

Financial technology capability is essential to offer end-to-end automation, real-time operations, transaction processing at scale, and meet regulatory obligations.